Published January 16, 2026

Trump’s 10% Credit Card Interest Rate Cap: What Banks Aren’t Saying—and Why It Could Quietly Reshape San Antonio Real Estate

THE POLICY THAT SOUNDS GOOD—UNTIL YOU FOLLOW THE MONEY

At first glance, a 10% cap on credit card interest rates sounds like a win for everyday Americans. Lower interest. Lower payments. More breathing room.

But here’s what most headlines miss:

Housing affordability isn’t driven by one number. It’s driven by access to credit, liquidity, and consumer behavior.

And that’s where this proposal could quietly ripple into the real estate market—especially in fast-growing cities like San Antonio, Texas, where affordability and migration trends are tightly linked.

Banks aren’t pushing back because they’re greedy.

They’re pushing back because credit systems don’t compress neatly without consequences.

And those consequences matter if you’re:

• A family planning a move

• A buyer watching mortgage rates

• A homeowner thinking long-term equity

WHAT TRUMP PROPOSED—AND WHY DETAILS MATTER

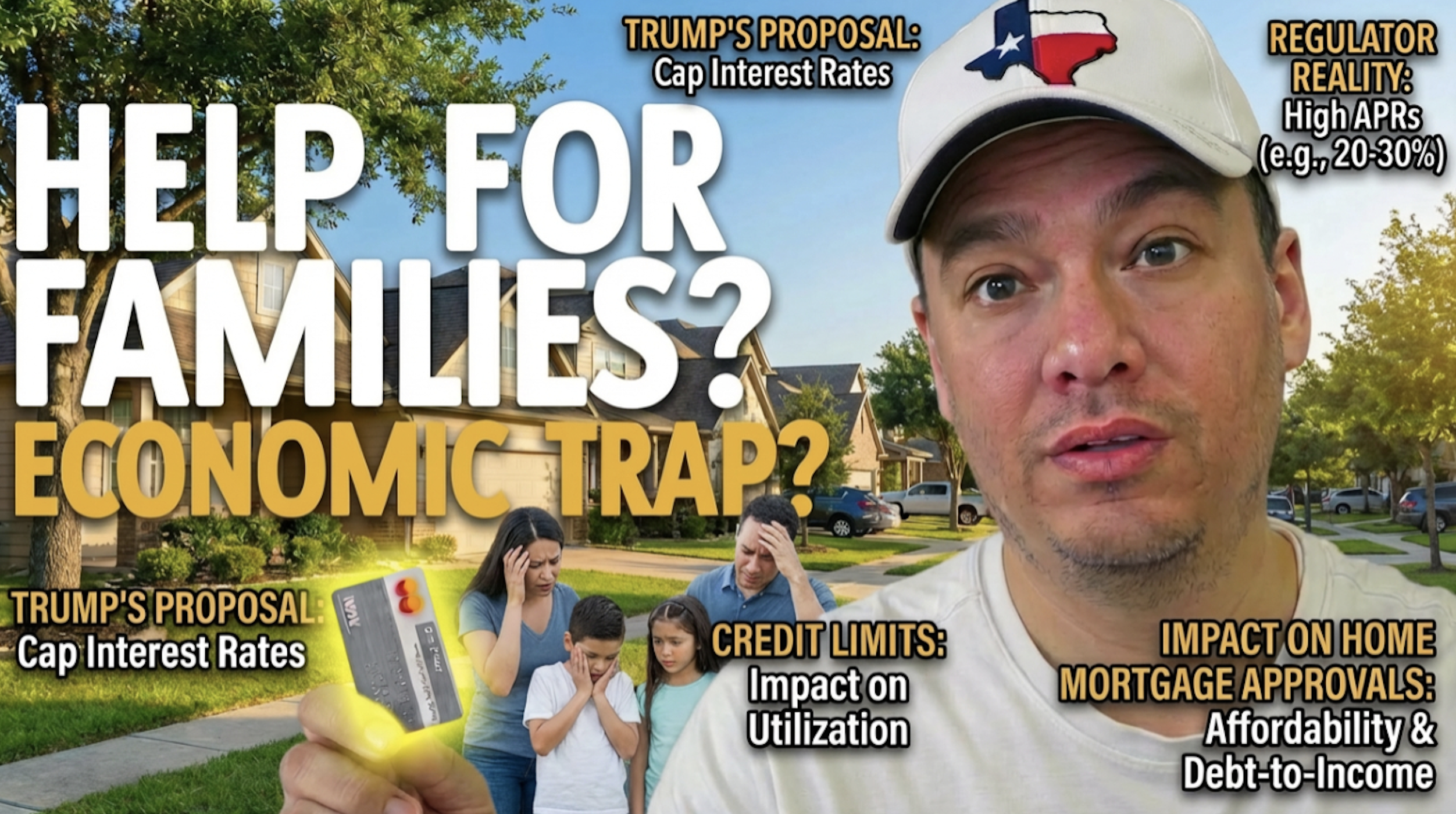

President Donald Trump has called for a one-year cap on credit card interest rates at 10%, starting January 20. The stated goal: ease cost-of-living pressure and restore affordability.

But there’s a major issue:

No enforcement mechanism has been defined.

No executive order.

No legislation.

No regulatory framework.

Industry analysts—including Morningstar—widely agree that Congress would likely need to act for such a cap to be enforceable.

That uncertainty alone is enough to make financial markets—and lenders—react defensively.

WHY BANKS ARE SOUNDING THE ALARM

According to the Electronic Payments Coalition, a 10% cap would severely restrict or eliminate access to credit for 82–88% of credit card holders, particularly those with scores below 740.

Why?

Because credit card lending isn’t priced just on interest—it’s priced on risk.

Subprime borrowers, moderate-income households, and small business owners would be the first affected.

Banks argue the result would be:

• Higher annual fees

• Fewer rewards programs

• Reduced credit limits

• Closed accounts

Which leads to something critical for real estate:

Reduced consumer liquidity.

THE HIDDEN LINK BETWEEN CREDIT CARDS AND HOME BUYING

Most people assume mortgages exist in isolation.

They don’t.

Credit cards influence:

• Debt-to-income ratios

• Emergency liquidity

• Down payment stability

• Buyer confidence

When access to revolving credit tightens, buyers pause—even if mortgage rates fall.

This is why lower rates don’t always translate into lower home prices.

WHAT THE DATA SHOWS RIGHT NOW

According to the CFPB:

• Average APRs hit 25.2% (general cards)

• Private label cards exceeded 31%

• Minimum-payment-only users are at the highest level since 2015

Banks argue that capping rates at 10% would make many credit portfolios mathematically unprofitable.

And when lending becomes unprofitable, lenders pull back.

WHAT HAPPENS WHEN CREDIT TIGHTENS?

Historically, tight consumer credit leads to:

• Slower consumer spending

• Reduced household mobility

• Delayed home purchases

• Increased rental demand

For San Antonio real estate, this matters deeply.

San Antonio thrives because:

• It remains affordable compared to Austin and Dallas

• It attracts families relocating for lifestyle value

• It benefits from stable employment sectors

But affordability is a system, not a headline.

SAN ANTONIO REAL ESTATE: WHY THIS CITY IS DIFFERENT

San Antonio is uniquely positioned during moments like this.

Why?

• Lower median home prices cushion affordability shocks

• Migration demand remains strong

• Military, healthcare, and manufacturing stabilize employment

• Buyers are often value-driven, not speculative

If credit tightens nationally, San Antonio becomes more attractive, not less—especially for families priced out of other Texas metros.

THE BANK EXECUTIVES’ WARNING—DECODED

Executives from JPMorgan, Citigroup, Bank of America, and Wells Fargo all agree on one thing:

Affordability matters.

But they argue blunt caps create credit rationing, not relief.

Jamie Dimon’s warning that subprime borrowers would be hit hardest matters because those same borrowers are often:

• First-time buyers

• Relocating families

• Workforce households

When those buyers lose access to flexible credit, housing demand shifts—not disappears.

WHAT THIS MEANS FOR SAN ANTONIO BUYERS

If this cap moves forward—or even threatens to—buyers who understand the system early gain leverage.

Smart buyers focus on:

• Stable budgeting

• Strategic timing

• Local market knowledge

• Long-term livability

Not just interest rates.

WHAT THIS MEANS FOR SELLERS

For sellers in San Antonio:

• Demand may concentrate in affordable neighborhoods

• Well-priced homes will outperform

• Move-in-ready properties gain premium appeal

Sellers who price with buyer psychology in mind will win.

THE BIG MISCONCEPTION MOST PEOPLE MISS

Lower interest rates ≠ cheaper homes

Credit caps ≠ affordability

Policy headlines ≠ local market reality

Real estate is local. Credit is emotional. Timing is strategic.

IF YOU ONLY REMEMBER ONE THING, REMEMBER THIS:

Affordability isn’t about forcing prices down—it’s about keeping families mobile, confident, and informed.

And that’s where San Antonio continues to shine.

WHY THIS BENEFITS SAN ANTONIO REAL ESTATE LONG-TERM

As national markets fluctuate:

• San Antonio remains stable

• Entry points stay accessible

• Long-term equity remains strong

• Family-driven demand continues

This city benefits when buyers prioritize value over hype.

FINAL THOUGHT

This isn’t about politics.

It’s about planning.

Families who understand how credit, policy, and local markets intersect make better long-term decisions.

And in San Antonio, those decisions still create opportunity.

Jesse Rene Garza

| Garza Home Team | Keller Williams City View

or another way